In a dramatic week that captured the tension between technological progress and human cost, Oracle Corporation (NYSE: ORCL) delivered record-breaking quarterly earnings while simultaneously executing the largest layoffs in its history. The tech giant's Q3 2026 results revealed a company undergoing profound transformation—cloud revenue surging 44%, AI infrastructure bookings exploding 243%, and a raised 2027 revenue outlook of $90 billion. Yet these financial triumphs came alongside termination emails sent to approximately 30,000 employees worldwide, a stark reminder of the human capital being reallocated to fuel Oracle's AI ambitions. For investors, this moment represents both opportunity and ethical calculus as one of technology's oldest giants bets its future on artificial intelligence.

Oracle's AI Bet Pays Off with Record Earnings But at Human Cost

Oracle's fiscal third-quarter results for 2026 delivered exactly what Wall Street had been hoping for—and then some. The company reported adjusted earnings per share of $1.79, beating analyst estimates of $1.70 by 5.3%, while revenue reached $17.2 billion versus the $16.92 billion forecast. More importantly, the numbers revealed the accelerating momentum of Oracle's cloud transformation. Total cloud revenue hit $8.9 billion, representing 44% year-over-year growth, with the cloud infrastructure segment alone soaring 84% to $4.9 billion.

Behind these numbers lies Oracle's aggressive push into artificial intelligence infrastructure. The company's AI infrastructure revenue grew an astonishing 243% year-over-year, while multicloud database revenue surged 531%. Perhaps most telling was the explosion in remaining performance obligations (RPO)—contractual commitments for future services—which ballooned to $553 billion, up 325% from the previous year. "We're seeing unprecedented demand for AI training and inference workloads," CEO Safra Catz told analysts, highlighting that Oracle's cloud infrastructure (OCI) is now handling some of the largest AI models in production.

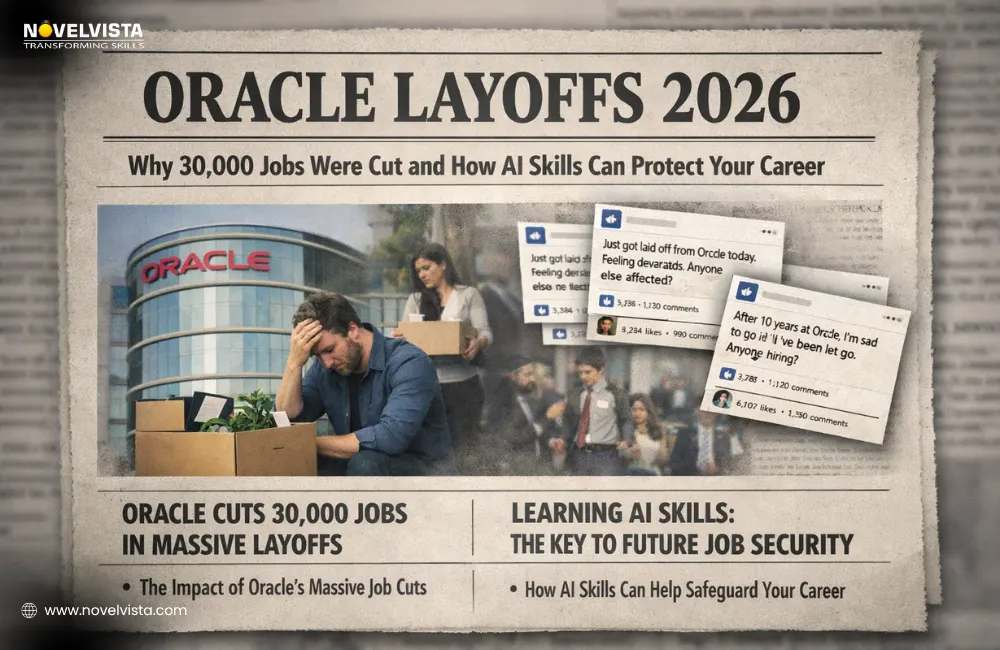

Yet this financial victory arrived alongside one of the most brutal workforce reductions in tech history. On March 31, 2026—just weeks after the earnings celebration—Oracle began notifying approximately 30,000 employees worldwide that their positions had been eliminated. The cuts represented roughly 18% of Oracle's 162,000-person workforce and were executed with brutal efficiency: termination emails arrived at 6 a.m. local time, with immediate system access revocation and no transition period.

From Earnings Beat to Mass Layoffs: The 72-Hour Transformation

The timeline of events reveals how rapidly Oracle pivoted from celebration to restructuring. On March 10, the company hosted its earnings call, with executives touting "the best quarter in Oracle's history" and raising 2027 revenue guidance to $90 billion. Analysts responded enthusiastically, with several raising price targets and praising the company's AI positioning. The stock jumped nearly 10% in after-hours trading.

Just three weeks later, on March 31, the layoffs began. Employees across the United States, India, Canada, Mexico, and other countries received identical emails from "Oracle Leadership" stating their roles had been "eliminated as part of a broader organizational change." The cuts hit particularly hard in India, where approximately 12,000 positions were eliminated—nearly 40% of Oracle's local workforce. Departments most affected included Oracle Health, Sales, Cloud, and NetSuite teams.

Investment bank TD Cowen estimated the layoffs would free up $8 to $10 billion in annual cash flow, which Oracle plans to redirect toward AI infrastructure expansion and data center construction. The company had already hinted at this strategy in its Q3 earnings report, noting "we have been restructuring our teams into more agile, AI-focused units." What employees and investors didn't anticipate was the scale and immediacy of the restructuring.

Why Investors Are Rewarding Oracle's Ruthless AI Pivot

Despite the human toll, financial markets have largely applauded Oracle's strategic moves. The stock maintained its post-earnings gains and analysts have generally maintained bullish outlooks. The average 12-month price target among 40 analysts sits at $262.91, with some as high as $400—representing potential upside of 117% from current levels around $146.

"Oracle is making the painful but necessary transition from a human-capital-intensive enterprise software company to an AI-infrastructure-as-a-service powerhouse," explained technology analyst Mark Murphy of Barclays. "The math is straightforward: each dollar shifted from payroll to AI infrastructure generates significantly higher returns in today's market." Murphy maintains an Overweight rating on ORCL with a $230 price target, noting that while he recently reduced his target from $310 due to macroeconomic concerns, the long-term thesis remains intact.

The investment case rests on several key pillars. First, Oracle's cloud infrastructure business is growing at nearly triple the rate of competitors like AWS and Azure in percentage terms, albeit from a smaller base. Second, the company's $553 billion RPO provides unprecedented revenue visibility—equivalent to more than eight years of current annual revenue. Third, Oracle's sovereign cloud offerings (government-compliant cloud environments) and embedded AI agents in Fusion applications create competitive moats that are difficult to replicate.

"What investors are recognizing is that Oracle isn't just participating in the AI boom—it's building the infrastructure that enables it," said Dan Ives of Wedbush Securities, who has a $298 price target on the stock. "The layoffs, while unfortunate, signal management's commitment to winning the AI infrastructure race at all costs."

Where Oracle Stands Now: Debt, Backlog, and Market Position

Oracle enters this new phase with significant financial strengths and challenges. The company carries approximately $125 billion in debt against a $500 billion backlog of contracted business. This leveraged position raises eyebrows among some analysts, but management argues the debt is manageable given the predictable revenue stream from cloud contracts.

The company's capital expenditure plans remain aggressive, with a $50 billion target for fiscal 2026 to expand data center capacity. Oracle currently operates 66 cloud regions worldwide and plans to add 20 more in the coming year, many specifically designed for AI workloads. This expansion is essential to accommodate the exploding demand—CEO Safra Catz noted that Oracle is "literally building data centers as fast as we can" to keep up with customer requirements.

Competitively, Oracle occupies a unique position bridging enterprise software and cloud infrastructure. While it trails AWS, Microsoft Azure, and Google Cloud in overall cloud market share, its focus on AI-specific infrastructure and enterprise integration gives it differentiated advantages. The multicloud strategy—particularly the Oracle Database@Google Cloud partnership—allows customers to run Oracle workloads on competing clouds while maintaining full compatibility.

"Oracle's secret weapon is its decades-long relationships with Fortune 500 companies," noted technology analyst Brent Thill of Jefferies. "When these enterprises embark on AI transformation, they naturally turn to vendors they already trust with their most critical data. Oracle's challenge is executing the technical transformation to match its relationship advantages."

The Road Ahead: Can Oracle Sustain Its AI Momentum?

The critical question for investors is whether Oracle's current momentum is sustainable or merely a cyclical spike in AI enthusiasm. Several factors suggest the growth has staying power. First, AI workloads are still in early adoption—industry estimates suggest only 10-15% of potential AI inference workloads have moved to cloud infrastructure. Second, Oracle's focus on "sovereign cloud" (data residency-compliant clouds) addresses growing regulatory concerns that could slow competitors.

However, risks abound. The $125 billion debt load creates vulnerability if interest rates remain elevated or if cloud growth slows. Competition is intensifying, with all major cloud providers investing heavily in AI chips and infrastructure. And the human capital reduction—while financially beneficial in the short term—could damage morale and innovation capacity over time.

"The next two quarters will be crucial," predicts analyst Keith Bachman of BMO Capital Markets. "We need to see if Oracle can continue beating cloud growth estimates while integrating its massive AI infrastructure investments. The layoffs bought them runway, but now they must deliver on the promise." Bachman maintains a Market Perform rating with a $210 price target.

For retail investors, the decision hinges on time horizon and risk tolerance. Short-term traders might find volatility around earnings announcements, while long-term investors must assess whether Oracle truly has a sustainable competitive advantage in AI infrastructure or is merely riding a wave.

Key Takeaways for Investors

Oracle's dramatic week reveals fundamental truths about investing in the AI era. First, financial markets continue to reward aggressive technological bets, even when they come at significant human cost. Second, the transition from traditional software to AI infrastructure creates both enormous opportunities and painful dislocations. Third, Oracle's unique position—bridging enterprise relationships with cloud infrastructure—gives it advantages but also requires flawless execution.

For those considering ORCL stock, the calculus involves weighing several factors: the $90 billion 2027 revenue target against current $146 share price, the $553 billion RPO providing unprecedented visibility, the $8-10 billion annual savings from layoffs being reinvested in growth, and the competitive threats from better-funded cloud giants. Most analysts see upside, with price targets suggesting 40-100% potential returns over the next 12-24 months.

As Oracle CEO Safra Catz reminded investors: "We're playing the long game here. The AI revolution is just beginning, and we're building the infrastructure that will power it for decades to come." Whether that vision justifies the human cost and financial risk is the essential question every investor must answer for themselves.