The Dow Jones Industrial Average experienced a rollercoaster year in 2024, marked by historic milestones, unexpected volatility, and a stark divergence between different investment strategies. The blue-chip index briefly touched the psychologically significant 40,000 level for the first time in May, fueled by optimism about cooling inflation and potential Federal Reserve rate cuts. However, the celebration was short-lived as the Dow retreated to close at 39,869 that same day, highlighting the fragile nature of market sentiment. While the index posted a respectable 6% year-to-date gain through May, it significantly lagged the broader S&P 500 and technology-heavy Nasdaq, setting the stage for a year where traditional value strategies faced headwinds.

The 40,000 Milestone: How Inflation Data Fueled a Historic Moment

On May 16, 2024, the Dow Jones Industrial Average crossed the 40,000 threshold for the first time in its 128-year history. The milestone came after a favorable April inflation report showed the Consumer Price Index climbing 3.4%—below analysts' expectations and indicating a clear trend toward decelerating price growth. "Following three months of inflation upsets, the April report put a soft landing and 2024 rate cut back in investors' sights," said Julia Pollak, ZipRecruiter's chief economist, in a statement to NBC News. The index, comprising 30 major U.S. companies including Apple and McDonald's, had gained a modest 6% on the year at that point, while the S&P 500 and Nasdaq Composite reached their own record highs with stronger year-to-date performances.

Timeline: Key Moments That Defined the Dow's 2024 Journey

The Dow's path through 2024 was anything but linear. After hitting 40,000 in May, the index surged again in July, adding more than 700 points in a single day to close at another record high. This rally was driven by strong corporate earnings and continued optimism about the economic outlook. However, the momentum shifted dramatically in December when the Federal Reserve delivered what markets perceived as a hawkish surprise. Despite cutting interest rates by a quarter percentage point, policymakers projected only two additional rate cuts for 2025—fewer than investors had anticipated. The reaction was immediate and severe: the Dow plunged over 1,100 points on December 18, marking one of its worst single-day declines of the year. The selloff continued through year-end, with the index closing down 400 points on December 30 as Wall Street limped into 2025.

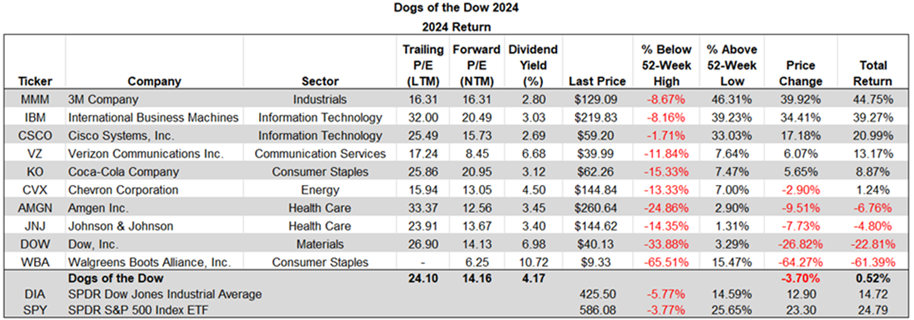

Why Value Strategies Struggled in a Growth-Oriented Market

One of the most telling stories of 2024 was the dramatic underperformance of the "Dogs of the Dow" strategy compared to the broader market. This approach, which involves investing equal amounts in the ten highest-yielding Dow stocks at the start of each year, lagged the Dow Jones Industrial Average by more than 14 full percentage points and trailed the S&P 500 by over 24 percentage points. "In years where the market generates returns that favor growth-oriented stocks, the Dogs of the Dow strategy has a tendency to lag," explained David I. Templeton, CFA, Principal and Portfolio Manager at HORAN Wealth. The 2024 market was dominated by megacap technology stocks and growth-oriented sectors, leaving dividend-focused value strategies in the dust. Particularly damaging was the Dow Dogs' holding in Walgreens Boots Alliance, which alone contributed a negative 12.94 percentage points to the strategy's total return.

Where the Dow Stands Now: Assessing the Damage and Recovery

Despite the December volatility, the Dow Jones Industrial Average managed to finish 2024 with a gain of approximately 12.9%, according to year-end market analysis. This performance, while positive, paled in comparison to the S&P 500's 23.3% surge and the Nasdaq's staggering 28.6% advance. The divergence highlights a market increasingly driven by a handful of technology giants rather than the broad-based industrial companies that comprise the Dow. As of late December, the index traded around 42,500—well above its 2024 starting point but significantly below the peak optimism of earlier in the year. Bond yields spiked following the Fed's December meeting, putting additional pressure on equity valuations and creating uncertainty about the sustainability of the bull market.

What Happens Next: Navigating the Fed's Shifting Policy Landscape

The Federal Reserve's unexpectedly hawkish stance in December has reshaped investor expectations for 2025. With only two projected rate cuts instead of the three or four many market participants had hoped for, borrowing costs may remain elevated for longer than anticipated. This environment presents both challenges and opportunities for Dow investors. Historically, periods of Fed tightening have favored quality companies with strong balance sheets and consistent cash flows—characteristics common among many Dow components. However, if economic growth slows more than expected, the index's concentration in cyclical industrial and financial stocks could become a liability. Investors should monitor inflation data closely, as any resurgence would likely delay rate cuts further and potentially trigger additional market volatility.

The Bottom Line: Key Lessons for Investors

The Dow Jones Industrial Average's 2024 performance offers several crucial insights for investors. First, milestone numbers like 40,000 are psychologically significant but don't necessarily indicate sustainable momentum. Second, in a market dominated by growth stocks, traditional value strategies can suffer dramatic underperformance—sometimes by 20 percentage points or more. Third, Federal Reserve policy remains the primary driver of market volatility, with even subtle shifts in language capable of triggering thousand-point swings. Finally, while the Dow provides exposure to America's industrial backbone, investors seeking broader market participation may need to look beyond this narrow index. As 2025 unfolds, maintaining a diversified portfolio and focusing on fundamentals rather than headlines will be more important than ever.